He Downward Slope of the Demand Curve Again Illustrates the Pattern .

Chapter 3. Demand and Supply

3.1 Demand, Supply, and Equilibrium in Markets for Goods and Services

Learning Objectives

By the finish of this section, you will exist able to:

- Explicate need, quantity demanded, and the constabulary of demand

- Identify a need bend and a supply curve

- Explain supply, quantity supply, and the law of supply

- Explain equilibrium, equilibrium toll, and equilibrium quantity

First let'southward kickoff focus on what economists hateful by demand, what they mean past supply, and so how need and supply collaborate in a marketplace.

Demand for Goods and Services

Economists use the term demand to refer to the amount of some good or service consumers are willing and able to purchase at each price. Need is based on needs and wants—a consumer may be able to differentiate between a need and a desire, only from an economist'due south perspective they are the same thing. Demand is besides based on ability to pay. If you cannot pay for it, you have no effective demand.

What a buyer pays for a unit of the specific good or service is called price. The total number of units purchased at that price is called the quantity demanded. A rise in price of a good or service nearly ever decreases the quantity demanded of that good or service. Conversely, a fall in price will increment the quantity demanded. When the price of a gallon of gasoline goes upward, for example, people wait for means to reduce their consumption by combining several errands, commuting by carpool or mass transit, or taking weekend or vacation trips closer to home. Economists telephone call this inverse relationship between price and quantity demanded the law of need. The constabulary of demand assumes that all other variables that touch on demand (to be explained in the next module) are held constant.

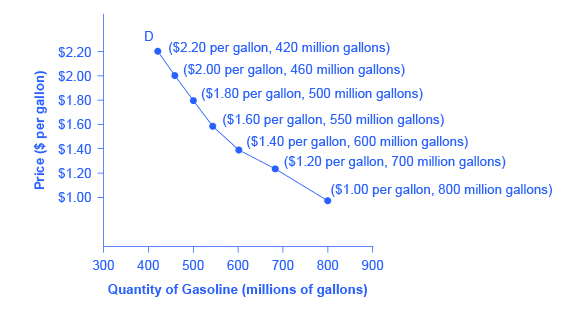

An example from the market for gasoline can exist shown in the form of a table or a graph. A table that shows the quantity demanded at each price, such as Table 1, is called a demand schedule. Cost in this instance is measured in dollars per gallon of gasoline. The quantity demanded is measured in millions of gallons over some time menses (for case, per day or per year) and over some geographic area (like a state or a country). A demand curve shows the relationship betwixt cost and quantity demanded on a graph like Effigy 1, with quantity on the horizontal centrality and the toll per gallon on the vertical centrality. (Note that this is an exception to the normal rule in mathematics that the independent variable (x) goes on the horizontal centrality and the dependent variable (y) goes on the vertical. Economics is not math.)

The need schedule shown by Table 1 and the demand curve shown past the graph in Figure 1 are ii ways of describing the same relationship between price and quantity demanded.

| Price (per gallon) | Quantity Demanded (millions of gallons) |

|---|---|

| $1.00 | 800 |

| $i.20 | 700 |

| $1.40 | 600 |

| $1.60 | 550 |

| $i.lxxx | 500 |

| $2.00 | 460 |

| $2.20 | 420 |

| Table 1. Cost and Quantity Demanded of Gasoline | |

Need curves will appear somewhat different for each product. They may appear relatively steep or apartment, or they may exist straight or curved. Nearly all demand curves share the cardinal similarity that they slope down from left to right. Then need curves embody the constabulary of demand: As the toll increases, the quantity demanded decreases, and conversely, as the price decreases, the quantity demanded increases.

Confused virtually these different types of demand? Read the adjacent Articulate It Up feature.

Is demand the same as quantity demanded?

In economic terminology, need is not the same as quantity demanded. When economists talk near need, they mean the relationship betwixt a range of prices and the quantities demanded at those prices, every bit illustrated by a demand curve or a demand schedule. When economists talk most quantity demanded, they mean only a certain indicate on the demand curve, or 1 quantity on the demand schedule. In short, need refers to the bend and quantity demanded refers to the (specific) point on the curve.

Supply of Appurtenances and Services

When economists talk most supply, they mean the amount of some good or service a producer is willing to supply at each price. Price is what the producer receives for selling ane unit of measurement of a good or service. A rise in price near e'er leads to an increment in the quantity supplied of that good or service, while a fall in cost will decrease the quantity supplied. When the toll of gasoline rises, for example, it encourages profit-seeking firms to take several actions: expand exploration for oil reserves; drill for more oil; invest in more than pipelines and oil tankers to bring the oil to plants where it can be refined into gasoline; build new oil refineries; purchase additional pipelines and trucks to ship the gasoline to gas stations; and open up more gas stations or proceed existing gas stations open longer hours. Economists call this positive relationship between price and quantity supplied—that a college price leads to a higher quantity supplied and a lower price leads to a lower quantity supplied—the law of supply. The constabulary of supply assumes that all other variables that touch supply (to be explained in the next module) are held constant.

Nevertheless unsure about the dissimilar types of supply? See the post-obit Articulate It Up feature.

Is supply the same as quantity supplied?

In economic terminology, supply is non the aforementioned as quantity supplied. When economists refer to supply, they mean the relationship between a range of prices and the quantities supplied at those prices, a human relationship that can be illustrated with a supply curve or a supply schedule. When economists refer to quantity supplied, they mean only a sure betoken on the supply curve, or 1 quantity on the supply schedule. In curt, supply refers to the curve and quantity supplied refers to the (specific) betoken on the curve.

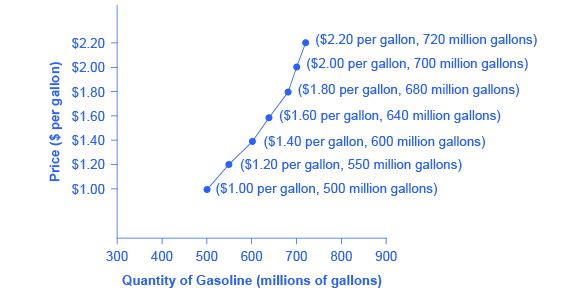

Effigy 2 illustrates the law of supply, again using the market for gasoline equally an example. Like demand, supply can be illustrated using a tabular array or a graph. A supply schedule is a table, similar Table ii, that shows the quantity supplied at a range of different prices. Over again, price is measured in dollars per gallon of gasoline and quantity supplied is measured in millions of gallons. A supply curve is a graphic illustration of the relationship between price, shown on the vertical axis, and quantity, shown on the horizontal axis. The supply schedule and the supply curve are just 2 different ways of showing the same data. Notice that the horizontal and vertical axes on the graph for the supply curve are the aforementioned every bit for the need bend.

| Cost (per gallon) | Quantity Supplied (millions of gallons) |

|---|---|

| $1.00 | 500 |

| $1.20 | 550 |

| $i.40 | 600 |

| $1.sixty | 640 |

| $i.80 | 680 |

| $2.00 | 700 |

| $2.xx | 720 |

| Tabular array two. Price and Supply of Gasoline | |

The shape of supply curves will vary somewhat according to the product: steeper, flatter, straighter, or curved. Virtually all supply curves, however, share a basic similarity: they gradient upward from left to right and illustrate the constabulary of supply: every bit the cost rises, say, from $one.00 per gallon to $2.20 per gallon, the quantity supplied increases from 500 gallons to 720 gallons. Conversely, as the price falls, the quantity supplied decreases.

Equilibrium—Where Demand and Supply Intersect

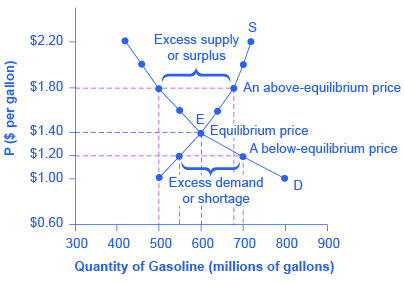

Considering the graphs for demand and supply curves both have toll on the vertical centrality and quantity on the horizontal axis, the demand bend and supply curve for a particular skillful or service can appear on the aforementioned graph. Together, need and supply determine the price and the quantity that will exist bought and sold in a market.

Figure 3 illustrates the interaction of demand and supply in the market place for gasoline. The need curve (D) is identical to Effigy 1. The supply curve (S) is identical to Effigy 2. Table 3 contains the same information in tabular form.

| Toll (per gallon) | Quantity demanded (millions of gallons) | Quantity supplied (millions of gallons) |

|---|---|---|

| $1.00 | 800 | 500 |

| $ane.20 | 700 | 550 |

| $1.twoscore | 600 | 600 |

| $1.60 | 550 | 640 |

| $one.fourscore | 500 | 680 |

| $ii.00 | 460 | 700 |

| $2.20 | 420 | 720 |

| Tabular array 3. Price, Quantity Demanded, and Quantity Supplied | ||

Recall this: When two lines on a diagram cross, this intersection usually ways something. The point where the supply curve (Due south) and the demand curve (D) cantankerous, designated by point Due east in Figure 3, is called the equilibrium. The equilibrium price is the only price where the plans of consumers and the plans of producers hold—that is, where the amount of the product consumers want to buy (quantity demanded) is equal to the amount producers want to sell (quantity supplied). This mutual quantity is chosen the equilibrium quantity. At whatsoever other price, the quantity demanded does not equal the quantity supplied, and so the market place is not in equilibrium at that price.

In Figure iii, the equilibrium price is $i.40 per gallon of gasoline and the equilibrium quantity is 600 million gallons. If you had just the need and supply schedules, and not the graph, y'all could find the equilibrium past looking for the price level on the tables where the quantity demanded and the quantity supplied are equal.

The give-and-take "equilibrium" means "remainder." If a market is at its equilibrium price and quantity, and so it has no reason to motility away from that point. Yet, if a market is not at equilibrium, then economic pressures arise to movement the market toward the equilibrium cost and the equilibrium quantity.

Imagine, for case, that the price of a gallon of gasoline was in a higher place the equilibrium toll—that is, instead of $1.forty per gallon, the toll is $1.fourscore per gallon. This above-equilibrium cost is illustrated by the dashed horizontal line at the price of $i.80 in Figure 3. At this higher price, the quantity demanded drops from 600 to 500. This decline in quantity reflects how consumers react to the higher toll by finding ways to use less gasoline.

Moreover, at this college price of $1.80, the quantity of gasoline supplied rises from the 600 to 680, as the college toll makes it more than profitable for gasoline producers to expand their output. At present, consider how quantity demanded and quantity supplied are related at this above-equilibrium cost. Quantity demanded has fallen to 500 gallons, while quantity supplied has risen to 680 gallons. In fact, at any above-equilibrium cost, the quantity supplied exceeds the quantity demanded. We call this an excess supply or a surplus.

With a surplus, gasoline accumulates at gas stations, in tanker trucks, in pipelines, and at oil refineries. This accumulation puts pressure on gasoline sellers. If a surplus remains unsold, those firms involved in making and selling gasoline are not receiving enough cash to pay their workers and to comprehend their expenses. In this state of affairs, some producers and sellers volition want to cutting prices, considering it is better to sell at a lower price than not to sell at all. Once some sellers commencement cutting prices, others will follow to avert losing sales. These price reductions in plough will stimulate a higher quantity demanded. So, if the price is in a higher place the equilibrium level, incentives congenital into the structure of demand and supply volition create pressures for the price to fall toward the equilibrium.

Now suppose that the toll is beneath its equilibrium level at $1.20 per gallon, every bit the dashed horizontal line at this price in Effigy 3 shows. At this lower price, the quantity demanded increases from 600 to 700 equally drivers take longer trips, spend more minutes warming upwards the car in the driveway in wintertime, terminate sharing rides to work, and buy larger cars that get fewer miles to the gallon. Withal, the below-equilibrium price reduces gasoline producers' incentives to produce and sell gasoline, and the quantity supplied falls from 600 to 550.

When the price is below equilibrium, in that location is excess demand, or a shortage—that is, at the given toll the quantity demanded, which has been stimulated by the lower price, now exceeds the quantity supplied, which had been depressed past the lower price. In this state of affairs, eager gasoline buyers mob the gas stations, only to find many stations running short of fuel. Oil companies and gas stations recognize that they have an opportunity to make college profits by selling what gasoline they have at a college cost. As a upshot, the toll rises toward the equilibrium level. Read Demand, Supply, and Efficiency for more give-and-take on the importance of the need and supply model.

Cardinal Concepts and Summary

A demand schedule is a table that shows the quantity demanded at unlike prices in the market. A demand curve shows the relationship between quantity demanded and cost in a given market on a graph. The police force of demand states that a higher toll typically leads to a lower quantity demanded.

A supply schedule is a table that shows the quantity supplied at different prices in the market place. A supply curve shows the human relationship between quantity supplied and price on a graph. The police force of supply says that a higher price typically leads to a college quantity supplied.

The equilibrium price and equilibrium quantity occur where the supply and demand curves cross. The equilibrium occurs where the quantity demanded is equal to the quantity supplied. If the price is below the equilibrium level, and then the quantity demanded volition exceed the quantity supplied. Backlog demand or a shortage will exist. If the price is above the equilibrium level, then the quantity supplied will exceed the quantity demanded. Excess supply or a surplus will exist. In either case, economical pressures will push the toll toward the equilibrium level.

Self-Check Questions

Review Effigy iii. Suppose the toll of gasoline is $1.60 per gallon. Is the quantity demanded higher or lower than at the equilibrium price of $1.forty per gallon? And what virtually the quantity supplied? Is there a shortage or a surplus in the market? If so, of how much?

Review Questions

- What determines the level of prices in a market?

- What does a downward-sloping demand curve mean almost how buyers in a marketplace will react to a college price?

- Will demand curves accept the same verbal shape in all markets? If not, how volition they differ?

- Volition supply curves take the aforementioned shape in all markets? If non, how will they differ?

- What is the relationship between quantity demanded and quantity supplied at equilibrium? What is the human relationship when there is a shortage? What is the relationship when there is a surplus?

- How can you lot locate the equilibrium point on a need and supply graph?

- If the cost is above the equilibrium level, would yous predict a surplus or a shortage? If the cost is below the equilibrium level, would you predict a surplus or a shortage? Why?

- When the cost is in a higher place the equilibrium, explain how market forces move the marketplace price to equilibrium. Do the aforementioned when the price is below the equilibrium.

- What is the departure between the demand and the quantity demanded of a product, say milk? Explain in words and bear witness the difference on a graph with a demand bend for milk.

- What is the divergence between the supply and the quantity supplied of a production, say milk? Explain in words and show the difference on a graph with the supply curve for milk.

Critical Thinking Questions

- Review Figure 3. Suppose the government decided that, since gasoline is a necessity, its price should be legally capped at $1.xxx per gallon. What do yous anticipate would be the consequence in the gasoline marketplace?

- Explain why the following statement is faux: "In the goods market, no heir-apparent would exist willing to pay more than the equilibrium price."

- Explain why the following statement is imitation: "In the appurtenances market, no seller would exist willing to sell for less than the equilibrium price."

Problems

Review Figure 3 again. Suppose the toll of gasoline is $1.00. Will the quantity demanded be lower or college than at the equilibrium price of $1.40 per gallon? Will the quantity supplied exist lower or higher? Is at that place a shortage or a surplus in the market? If so, of how much?

References

Costanza, Robert, and Lisa Wainger. "No Accounting For Nature: How Conventional Economics Distorts the Value of Things." The Washington Post. September 2, 1990.

European Committee: Agriculture and Rural Development. 2013. "Overview of the CAP Reform: 2014-2024." Accessed April 13, 205. http://ec.europa.european union/agriculture/cap-post-2013/.

Radford, R. A. "The Economic Organisation of a P.O.W. Camp." Economica. no. 48 (1945): 189-201. http://www.jstor.org/stable/2550133.

Glossary

- demand curve

- a graphic representation of the human relationship between toll and quantity demanded of a certain expert or service, with quantity on the horizontal axis and the toll on the vertical centrality

- demand schedule

- a table that shows a range of prices for a sure expert or service and the quantity demanded at each price

- need

- the human relationship betwixt toll and the quantity demanded of a certain good or service

- equilibrium price

- the price where quantity demanded is equal to quantity supplied

- equilibrium quantity

- the quantity at which quantity demanded and quantity supplied are equal for a certain toll level

- equilibrium

- the situation where quantity demanded is equal to the quantity supplied; the combination of price and quantity where there is no economical pressure from surpluses or shortages that would cause cost or quantity to modify

- excess demand

- at the existing price, the quantity demanded exceeds the quantity supplied; besides chosen a shortage

- excess supply

- at the existing price, quantity supplied exceeds the quantity demanded; also called a surplus

- police of demand

- the common relationship that a higher price leads to a lower quantity demanded of a certain expert or service and a lower toll leads to a higher quantity demanded, while all other variables are held constant

- law of supply

- the common relationship that a college cost leads to a greater quantity supplied and a lower price leads to a lower quantity supplied, while all other variables are held constant

- cost

- what a buyer pays for a unit of the specific expert or service

- quantity demanded

- the total number of units of a good or service consumers are willing to purchase at a given price

- quantity supplied

- the total number of units of a good or service producers are willing to sell at a given price

- shortage

- at the existing price, the quantity demanded exceeds the quantity supplied; also called excess demand

- supply bend

- a line that shows the relationship between price and quantity supplied on a graph, with quantity supplied on the horizontal axis and cost on the vertical axis

- supply schedule

- a table that shows a range of prices for a good or service and the quantity supplied at each cost

- supply

- the relationship between toll and the quantity supplied of a sure skillful or service

- surplus

- at the existing toll, quantity supplied exceeds the quantity demanded; likewise called excess supply

Solutions

Answers to Self-Check Questions

Since $1.60 per gallon is above the equilibrium cost, the quantity demanded would exist lower at 550 gallons and the quantity supplied would exist higher at 640 gallons. (These results are due to the laws of demand and supply, respectively.) The consequence of lower Qd and higher Qs would be a surplus in the gasoline market place of 640 – 550 = 90 gallons.

Source: https://opentextbc.ca/principlesofeconomics/chapter/3-1-demand-supply-and-equilibrium-in-markets-for-goods-and-services/

{kind=link}

Post a Comment for "He Downward Slope of the Demand Curve Again Illustrates the Pattern ."